Kelly Criterion vs. Dynamic Bankroll Adjustment

When deciding how much to bet, two popular strategies stand out: Kelly Criterion and Dynamic Bankroll Adjustment. Both aim to manage risk and grow your bankroll, but they differ in approach. Here's a quick breakdown:

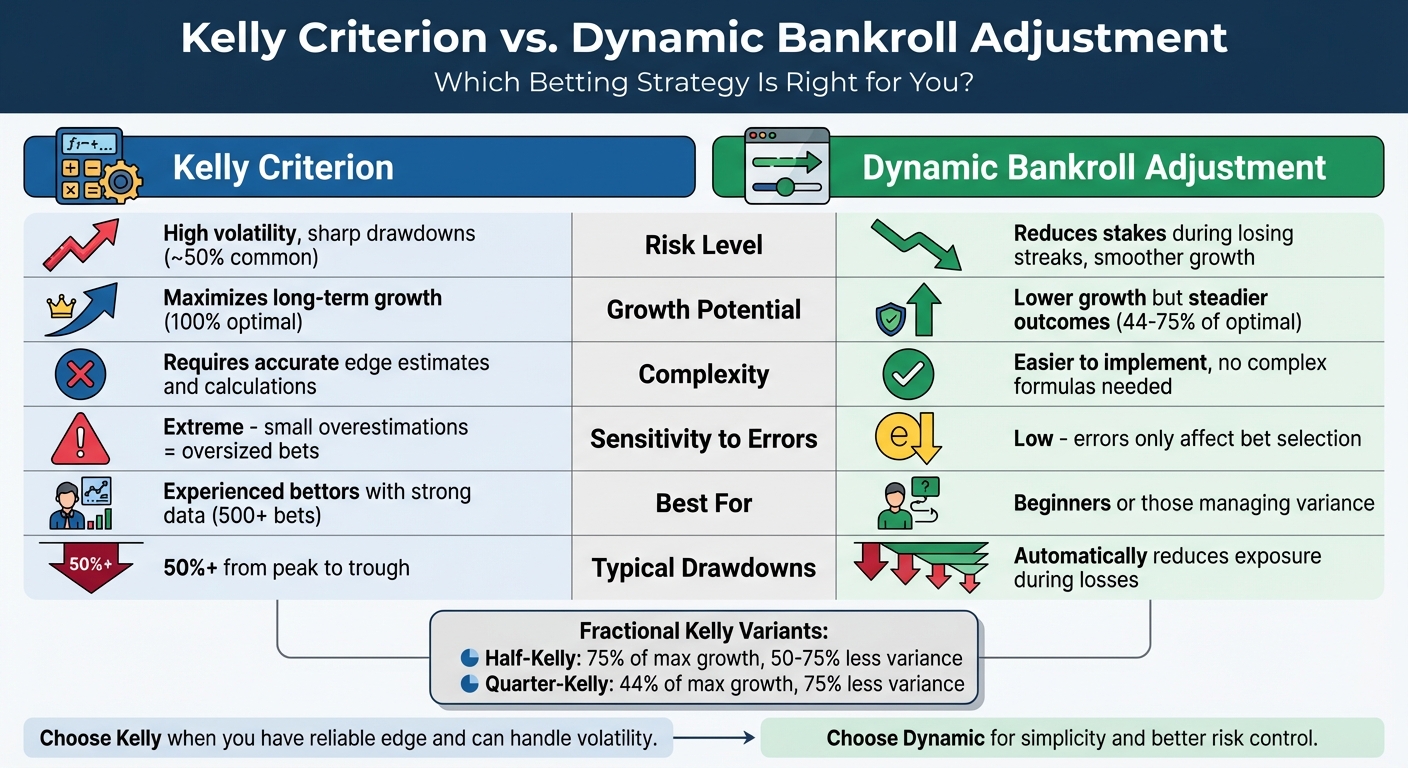

- Kelly Criterion: A formula that calculates the optimal percentage of your bankroll to bet based on your edge and odds. It’s designed to maximize long-term growth but comes with high volatility and requires precise probability estimates.

- Dynamic Bankroll Adjustment: A simpler method that adjusts bet sizes as a percentage of your current bankroll. It reduces stakes during losses and increases them after wins, offering smoother growth but lower maximum returns.

Quick Comparison

| Feature | Kelly Criterion | Dynamic Bankroll Adjustment |

|---|---|---|

| Risk | Higher volatility, sharp drawdowns | Reduces stakes during losing streaks |

| Growth Potential | Maximizes long-term growth | Lower growth but steadier outcomes |

| Complexity | Requires accurate edge estimates | Easier to implement |

| Best For | Experienced bettors with strong data | Beginners or those managing variance |

Choose Kelly when you have a reliable edge and can handle volatility. Opt for Dynamic Adjustment if you prefer simplicity and better risk control.

Kelly Criterion vs Dynamic Bankroll Adjustment: Complete Comparison Guide

Pro Bettors: Bankroll Management Strategy | Kelly Criterion | Betting Network

What Is the Kelly Criterion?

The Kelly Criterion is a mathematical approach to determine the ideal percentage of your bankroll to wager on a single bet. Introduced in 1956, this formula is designed to maximize long-term growth while managing risk. If the formula produces a result of zero or a negative number, it signals that the bet isn’t worth taking.

"The Kelly Criterion is a formula for sizing a sequence of bets by maximizing the long-term expected value of the logarithm of wealth." – Wikipedia

At its core, the Kelly Criterion balances two goals: growing your bankroll efficiently and avoiding the risk of losing it all. However, it’s not a shortcut to guaranteed profits. To benefit, you must identify bets with a positive expected value (+EV).

The Kelly Formula Explained

The formula is as follows:

f* = (b·p – q) / b

Here’s what each variable means:

- f*: The percentage of your bankroll to wager.

- b: The net odds (decimal odds minus 1).

- p: Your estimated probability of winning.

- q: The probability of losing (1 – p).

The numerator, b·p – q, represents your edge. A larger edge results in a bigger recommended bet size. The denominator, b, accounts for the odds - higher odds on underdogs lead to smaller suggested bets due to increased variance.

Let’s break it down with an example. Imagine an NFL underdog with +150 American odds (equivalent to 2.50 in decimal) and a 45% win probability. The net odds (b) are 1.50. Plugging into the formula: (0.45 × 1.50 – 0.55) / 1.50 ≈ 0.0833. This suggests betting about 8.33% of your bankroll - roughly $833 if your bankroll is $10,000.

Accurate win probability estimates are critical. Overestimating your edge, even slightly, can lead to excessive bets that put your bankroll at risk. To manage this, many bettors use a fractional version of the Kelly Criterion to reduce volatility.

Fractional Kelly Variants

Fractional Kelly is a more conservative approach that involves betting only a portion of the amount calculated by the full Kelly formula. Popular options include Half-Kelly (50% of the recommended stake) and Quarter-Kelly (25%). These variations aim to reduce volatility while still achieving meaningful growth.

For instance, Half-Kelly captures around 75% of the maximum growth rate while cutting variance by 50% to 75%. Quarter-Kelly, on the other hand, achieves about 44% of the maximum growth while reducing variance by roughly 75%. While Full Kelly betting is mathematically optimal, it often leads to significant drawdowns - up to 50% from peak to trough. Betting more than the Kelly-recommended amount can even eliminate growth entirely.

In a January 2026 simulation with a $1,000 bankroll and even-money bets at a 55% win rate, Full Kelly suggested betting 10% (or $100) per wager. While this strategy delivered the highest potential final bankroll, it also resulted in the widest range of outcomes and the steepest drawdowns compared to a 25% Kelly approach.

These fractional methods provide a balance between growth and risk, setting the stage for further benefits.

Benefits of the Kelly Criterion

The Kelly Criterion is unmatched in its ability to maximize long-term growth - provided your edge estimates are accurate. It also enforces discipline by steering you away from bets with zero or negative expected value, reducing the chance of depleting your bankroll.

One of its standout features is its adaptability. Since the formula calculates wagers as a percentage of your current bankroll, your bet sizes automatically adjust. After a win, your stakes increase; after a loss, they decrease, helping to protect your capital during tough stretches. Many professionals also suggest capping individual wagers at 2% to 5% of your bankroll to safeguard against unforeseen risks and estimation errors.

That said, the criterion assumes you have precise knowledge of the true win probability - a challenging ideal in sports betting, where probabilities are always estimates.

What Is Dynamic Bankroll Adjustment?

The Kelly Criterion uses a fixed formula to determine bet sizes based on your edge and bankroll, but dynamic bankroll adjustment takes it a step further. Instead of sticking to static calculations, this method continuously updates your stakes in real time, adjusting for changes in your bankroll and live odds. It’s particularly handy for live betting, where odds can shift quickly and unpredictably.

How Dynamic Adjustments Work

Dynamic systems rely on the Kelly formula - f* = (b·p – q) / b - but with a twist. These systems update the inputs constantly as conditions change. For instance, if an underdog’s odds shorten from +200 to +150 mid-game, the system recalculates your edge and adjusts your recommended stake accordingly.

Bettors often use a fractional multiplier (like 0.25 or 0.5) to smooth out the stakes based on recent performance. Volatility targeting is another key element, where stakes are scaled by comparing target volatility to actual volatility. For example, if your bankroll sees a 15% drawdown, the system automatically reduces your Kelly fraction by half to protect your capital. At a 25% drawdown, the system goes further, freezing new bet types and running diagnostics to recalibrate.

"At -15% [drawdown]: halve Kelly fraction; at -25%: freeze new bet types, run calibration & CLV diagnostics." - Sports-AI.dev

This real-time recalibration is what makes dynamic adjustment so effective, especially when paired with other risk management tools.

Core Features of Dynamic Adjustment

Dynamic adjustment relies on a few standout features to keep things running smoothly:

- Automatic scaling: Your bet sizes are recalculated after every win or loss, so you don’t have to make manual adjustments. Live data integration ensures the system stays updated with the latest odds and probabilities.

- Adaptive thresholding: During drawdowns, the system raises the minimum edge requirement (e.g., from 3% to 5%) to focus only on high-confidence bets. This helps avoid unnecessary risks during tough periods.

- Exposure caps: To prevent overexposure, many systems limit total risk to a certain percentage of your bankroll - typically around 20% to 25%. This protects against unexpected correlations or rare market events.

Benefits of Dynamic Adjustment

One of the biggest perks of dynamic adjustment is its ability to adapt on the fly. In fast-paced live betting, it automatically adjusts your stakes as odds change, so you’re less likely to overcommit based on outdated information or miss potential opportunities.

This approach also helps manage risk during losing streaks. By reducing stakes and enforcing strict drawdown protocols, dynamic adjustment minimizes the chance of blowing through your bankroll. It’s a disciplined way to ride out swings in variance and position yourself to take advantage when your edge reappears.

Another advantage is the system’s ability to account for real-time data and factors like slippage (the gap between displayed odds and actual execution prices). This makes it especially effective for live, in-play betting and prediction markets, where conditions can change in an instant.

Main Differences Between Kelly Criterion and Dynamic Bankroll Adjustment

Both the Kelly Criterion and dynamic bankroll adjustment aim to manage risk and grow your bankroll, but they approach the task in distinct ways. The Kelly Criterion relies on a mathematical formula, using estimated edge and odds to calculate bet sizes. On the other hand, dynamic bankroll adjustment bases its stake sizes on the current bankroll and recent outcomes, making it more reactive to real-time performance.

One major difference is how they handle errors in probability estimates. The Kelly Criterion is highly sensitive to inaccuracies - overestimating probabilities even slightly can lead to bets that are far too large, risking severe losses over time. If you go beyond the recommended Kelly stake, you can negate growth entirely and even face eventual ruin. Dynamic bankroll adjustment, however, avoids this problem by using a fixed percentage of the bankroll for stakes, which doesn't depend on precise edge calculations.

Volatility is another key distinction. The Kelly Criterion can lead to sharp fluctuations, with drawdowns exceeding 50% being relatively common. Dynamic bankroll adjustment, by contrast, helps smooth out the growth curve by reducing stakes during losing streaks and increasing them after wins.

In terms of adaptability, the Kelly Criterion excels at responding to live odds and edges. If your edge disappears, the formula will signal that you should skip the bet entirely. Dynamic systems, however, adjust risk based on the overall performance of your betting campaign rather than individual odds.

Here’s a table that breaks down these differences:

Side-by-Side Comparison

| Feature | Kelly Criterion | Dynamic Bankroll Adjustment |

|---|---|---|

| Formula Dependency | High; requires accurate win probability and odds | Low; uses a fixed percentage of the bankroll |

| Sensitivity to Errors | Extreme; overestimations can lead to significantly oversized bets | Low; errors only affect bet selection rather than stake size |

| Volatility Handling | High; aggressive swings with 50%+ drawdowns common | Moderate; smooths growth during losing streaks |

| Adaptability to Live Odds | High; adjusts instantly with changes in the perceived edge | Very high; responds to both odds and overall campaign performance |

| Risk of Ruin | Theoretically low, but high in practice if probabilities are overestimated | Very low; stakes shrink automatically as the bankroll declines |

| Key Objective | Maximize long-term growth rate | Balance growth with stability and survival |

Advantages and Disadvantages of Each Method

Let’s break down the strengths and weaknesses of these two strategies to see how they stack up.

The Kelly Criterion is known for optimizing long-term growth. It adjusts wager sizes based on the size of the edge, meaning bigger advantages lead to larger bets, while smaller edges result in smaller stakes. This method also acts as a safeguard by rejecting bets with no positive expected value, as the formula will yield zero or negative outcomes for such scenarios.

But here’s the catch: Kelly’s precision comes with significant risk. It’s notorious for its extreme volatility, with drawdowns of around 50% being fairly common. Even small errors in estimating probabilities can lead to oversized bets that amplify risks. As Market Math aptly put it, "The math of finding edge is simple. The math of sizing it correctly is what keeps you in the game". This strategy also demands accurate calculations, which can be challenging for many.

On the other hand, Dynamic Bankroll Adjustment offers a simpler, more forgiving alternative. It doesn’t require precise calculations and automatically reduces stakes during losing streaks, preserving capital. The psychological toll is also far less intense since it avoids the dramatic swings associated with Kelly betting.

However, this simplicity comes at a cost. Dynamic adjustment doesn’t differentiate between bets with varying levels of confidence, treating all positive-value bets the same. As a result, it often leaves potential profits untapped, particularly on high-edge opportunities. While it provides steadier growth, it doesn’t achieve the same theoretical maximum returns as the Kelly Criterion.

Pros and Cons Summary

| Method | Advantages | Disadvantages |

|---|---|---|

| Kelly Criterion | • Maximizes long-term growth rate • Adjusts stakes based on edge size • Filters out negative-value bets • Reduces time to double bankroll |

• High volatility with ~50% drawdowns • Sensitive to estimation errors • Psychologically stressful • Requires precise edge calculations |

| Dynamic Bankroll Adjustment | • Simple and easy to use • Automatically reduces stakes during losses • Encourages discipline and capital protection • Lower psychological stress |

• Doesn’t maximize growth • Treats all bets equally, regardless of edge • Slower growth compared to optimal strategies • Misses high-value opportunities |

When to Use Each Strategy

Deciding between the Kelly Criterion and dynamic bankroll adjustment comes down to factors like your confidence in having an edge, your comfort with risk, and how complex you want your system to be.

Choose the Kelly Criterion if you have a well-established edge supported by a large data sample, such as 500 bets or more. If your probability estimates are accurate and you’re prepared for potential drawdowns, Kelly can help you achieve maximum long-term growth. This method is ideal for independent bets, where you can validate your edge using metrics like Closing Line Value (CLV). As Juanse Brito, CEO & Co-Founder of Bet Hero, explains:

"Kelly is a sizing tool, not an edge-finding tool. If you don't have positive expected value, no amount of clever staking will make you profitable".

Opt for dynamic bankroll adjustment if you’re new to betting, unsure about your probability estimates, or prefer to avoid high volatility. This strategy works particularly well for multiple simultaneous bets or correlated outcomes, such as betting on a team to win and a player from that team to score. It’s also a safer option in markets with low liquidity or when platform fees reduce your edge.

Many experienced bettors adopt fractional Kelly (e.g., Half-Kelly or Quarter-Kelly) to balance growth and risk. Half-Kelly captures around 75% of the maximum growth rate while cutting variance by half. Quarter-Kelly is even more cautious, delivering about 44% of optimal growth while reducing variance by 75%.

Both strategies require specific tools to ensure they’re implemented correctly, as outlined below.

Requirements for Each Strategy

To use the Kelly Criterion effectively, you’ll need:

- Reliable probability models to make accurate predictions

- De-vigging calculators to eliminate sportsbook margins

- Real-time bankroll tracking software for precise calculations

- A Kelly calculator to minimize manual errors

- A detailed betting journal to track metrics like ROI and CLV, confirming your edge

Platforms like WagerProof offer professional-level tools and statistical models to help generate accurate probability estimates and verify your edge through closing line analysis.

For dynamic bankroll adjustment, you’ll need:

- Bankroll tracking software to apply your chosen percentage consistently after each bet

- A results log to monitor your overall performance

- Portfolio management tools to limit total exposure to 20–25% of your bankroll

These tools ensure you apply each approach consistently and align it with your broader betting strategy.

Conclusion

Both strategies focus on adjusting bet sizes, but they do so in distinct ways. The Kelly criterion aims for long-term growth by relying on precise probability estimates, while dynamic adjustment strategies prioritize safety by continuously recalibrating bet sizes. When you have accurate probability estimates - validated through strong data and CLV (Closing Line Value) analysis - Kelly can maximize growth. On the other hand, fractional Kelly approaches, like Half-Kelly or Quarter-Kelly, provide an added layer of safety by reducing the risk of extreme drawdowns.

"Kelly is a sharp tool when your probabilities are sound. Use it to size efficiently, apply Fractional Kelly for durability, and keep your edge estimates honest." - Bettored.org

Your choice of strategy should depend on factors like data accuracy, risk tolerance, and how you structure your bets. If your probability models are uncertain or you're managing multiple wagers at once, fractional Kelly approaches deliver smoother equity curves while still capturing 44–75% of the potential growth.

However, no strategy can succeed without accurate data. Without reliable probability inputs, de-vigged fair odds, and verified edge metrics, even the most advanced staking methods can backfire. As Market Math puts it:

"If you are guessing, the output is worse than useless because it gives you false confidence in a specific bet size".

The foundation of any effective bankroll strategy is access to transparent, accurate data. Tools like WagerProof offer the professional-grade data infrastructure needed for informed decisions. From prediction market analysis and statistical modeling to real-time CLV tracking and automated outlier detection, these platforms make systematic bankroll management possible. Whether you lean toward aggressive Kelly sizing or conservative dynamic adjustments, reliable data transforms your strategy into a path for consistent growth.

FAQs

How do I estimate win probability well enough to use Kelly?

To calculate win probability for the Kelly Criterion, start by evaluating your edge through historical data, player or team statistics, and market trends. Use statistical models to translate your insights into a probability estimate, and continuously adjust this as you gather more data and experience. Precision matters - if you overrate your edge, you might take on too much risk, but playing it too safe by underestimating could hold back your potential gains.

What Kelly fraction should I start with (half or quarter)?

Starting with a quarter Kelly (25%) is a safer approach, especially if you're unsure about your probability estimates or prefer to keep risk and volatility in check. While using a half Kelly (50%) can lead to higher growth, it also comes with a greater chance of experiencing significant losses. Opting for a smaller fraction, like 25%, strikes a balance between growth and safety, making it a sensible option for most bettors - particularly when you're still building confidence in your estimates.

How do I set drawdown rules and exposure caps for dynamic staking?

To manage risk effectively in dynamic staking, it's important to establish clear drawdown rules and exposure limits. Start by setting a maximum drawdown percentage - say, 10% - to cap potential losses. Then, decide on a maximum exposure per bet, typically 25-50% of your calculated Kelly stake.

Adjust your bet sizes dynamically based on your current bankroll, ensuring your total exposure always stays within these pre-defined limits. If your bankroll begins nearing the drawdown threshold, either reduce your stakes or pause betting altogether. This approach helps you protect your funds while maintaining a disciplined strategy.

Related Blog Posts

Ready to bet smarter?

WagerProof uses real data and advanced analytics to help you make informed betting decisions. Get access to professional-grade predictions for NFL, College Football, and more.

Get Started Free